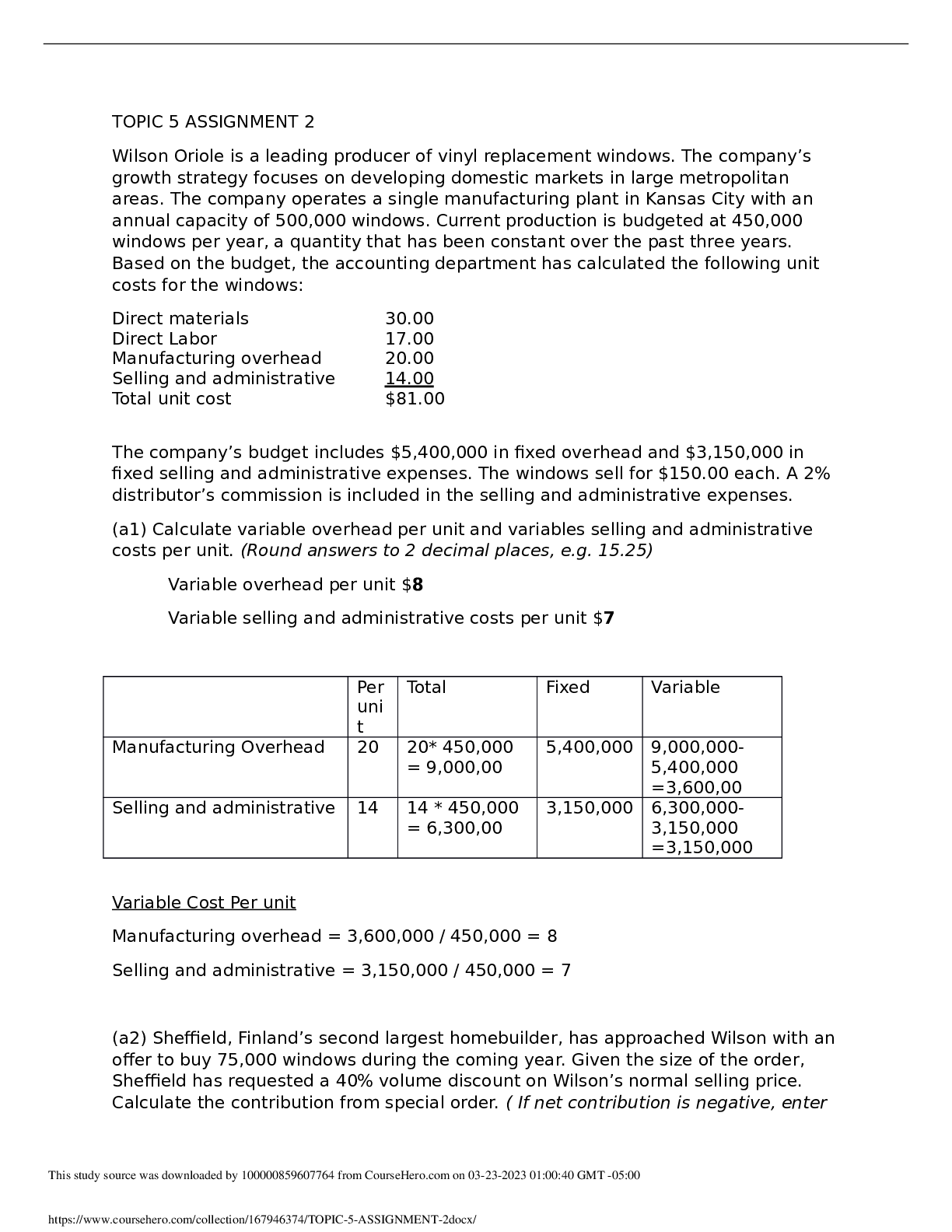

TOPIC 5 ASSIGNMENT 2

Wilson Oriole is a leading producer of vinyl replacement windows. The company’s

growth strategy focuses on developing domestic markets in large metropolitan

areas. The company operates a single ma

...

TOPIC 5 ASSIGNMENT 2

Wilson Oriole is a leading producer of vinyl replacement windows. The company’s

growth strategy focuses on developing domestic markets in large metropolitan

areas. The company operates a single manufacturing plant in Kansas City with an

annual capacity of 500,000 windows. Current production is budgeted at 450,000

windows per year, a quantity that has been constant over the past three years.

Based on the budget, the accounting department has calculated the following unit

costs for the windows:

Direct materials 30.00

Direct Labor 17.00

Manufacturing overhead 20.00

Selling and administrative 14.00

Total unit cost $81.00

The company’s budget includes $5,400,000 in fixed overhead and $3,150,000 in

fixed selling and administrative expenses. The windows sell for $150.00 each. A 2%

distributor’s commission is included in the selling and administrative expenses.

(a1) Calculate variable overhead per unit and variables selling and administrative

costs per unit. (Round answers to 2 decimal places, e.g. 15.25)

Variable overhead per unit $8

Variable selling and administrative costs per unit $7

Per

uni

t

Total Fixed Variable

Manufacturing Overhead 20 20* 450,000

= 9,000,00

5,400,000 9,000,000-

5,400,000

=3,600,00

Selling and administrative 14 14 * 450,000

= 6,300,00

3,150,000 6,300,000-

3,150,000

=3,150,000

Variable Cost Per unit

Manufacturing overhead = 3,600,000 / 450,000 = 8

Selling and administrative = 3,150,000 / 450,000 = 7

(a2) Sheffield, Finland’s second largest homebuilder, has approached Wilson with an

offer to buy 75,000 windows during the coming year. Given the size of the order,

Sheffield has requested a 40% volume discount on Wilson’s normal selling price.

Calculate the contribution from special order. ( If net contribution is negative, enter

amount with a negative sign, e.g. -5,285 or parentheses, e.g. (5,285). Round

answer to 0 decimal places, e.g. 8.971.)

Net contribution from special offer $(10,000)

Revised selling price per unit = 150 * (100 – 40%) = $90

Selling and administration distributor commission = 150 * 0.02 = $3

Selling and Administrative other variable costs = 14 – (3+7) = $4

Variable overhead = 3 + 4 = $7

Sales (150 * 60%) $90

Direct materials (30)

Direct labor (17)

Variable overhead (8)

Distributor’s commission ( 90*2%) (1.80)

Variable selling and administrative costs (4)

Contribution margin $29.20

Number of Units 75,000

Total contribution from special order $2,190,000

Contribution lost from regular sales

Sales $150

Direct materials (30)

Direct Labor (17)

Variable overhead (8)

Distributor’s commission (3)

Variable selling and administrative costs (4)

Contribution margin 88

Number of units (450,000 + 75,000 – 500,00) 25,000

Contribution lost from regular sales (88*25,000) (2,200,000)

Net contribution from special order (2,200,000-2,190,000) (10,000)

(c1) Return to the original data. Monk Builders has just signed a contract with the

state government to replace the windows in low-income housing units throughout

the state. Monk needs 80,000 windows to complete the job and has offered to buy

them from Wilson at a price of $110.00 per window. Monk will pick up the windows

at Wilson’s plant, so Wilson will not incur the $2 per window shipping charge. In

addition, Wilson will not need to pay a distributor’s commission, since the windows

will not be sold through a distributor.

Calculate the contribution from special order, contribution lost from regular sales

and the net contribution from special order.

Contribution from special order $4,240,000

Contribution lost from forgone regular sales $(2,640,00)

Net contribution from special order $1,600,00

Sales $110

Direct materials (30)

Direct Labor (17)

Variable overhead (8)

Variable selling and administrative costs (2)

Contribution Margin $53

Number of Units 80,000

Contribution from special order $4,240,000

Total Selling and Administrative costs 450,000 * 14 6,300,000

Less fixed selling and administrative costs 3,150,000

Total Variable Selling and Administrative Costs 3,150,000/

450,000 windows

$7 per window

Less costs not incurred on special depreciation

Commission 150*2% 3

Shipping 2

Variable selling & administrative costs per unit $2 per window

Contribution lost from regular sales

Sales 150

Direct materials (30)

Direct labor (17)

Variable overhead (8)

Distributor’s commission (3)

Variable selling & administrative costs (4)

Contribution margin 88

Number of units (450,000-80,000-500,000) 30,000

Contribution lost from regular sales (30,000*88) (2,640,000)

Net contribution from special order 1,600,000

(c2) Should Wilson accept Monk’s offer?

Wilson should accept Monk’s offer.

(d1) If Wilson decides to accept Monk’s offer, it will need to find an additional

30,000 windows to meet both the special order and normal sales. Sage Hill Panes

has offered to provide them to Wilson at a price of $130.00 per window. Sage Hill

Panes will deliver the windows to Wilson, and Wilson would then distribute them to

its customers.

Calculate total contribution from outsourcing.

Total contribution from outsourcing $390,000

Purchase Price (130)

Distribution (150*0.02) (3)

Variable selling & Administrative Costs (4)

Contribution Margin 13

Number of units 30,000

Contribution margin from outsourcing (30,000*13) 390,000

(d2) Should Wilson outsource the production of the extra windows to Sage Hill

Panes? Yes

[Show More]