Financial Accounting > Class Notes > Audit Glossary (All)

Audit Glossary

Document Content and Description Below

Last updated: 3 years ago

Preview 1 out of 7 pages

Instant download

Buy this Document to get the Full Access Instantly

Provided by Students Who Aced it

We Verify Document Content to Gurantee Accuracy

Reviews( 0 )

Document information

Connected school, study & course

About the document

Uploaded On

Jul 07, 2020

Number of pages

7

Written in

All

Additional information

This document has been written for:

Uploaded

Jul 07, 2020

Downloads

0

Views

225

Document Keyword Tags

Recommended For You

Get more on Class Notes »

Financial Accounting with International Financial Reporting St...

Solutions Manual for Advanced Accounting, 8th Edition by Debra...

Advanced Accounting 4th Edition By Hamlen, Huefner, Largay (Te...

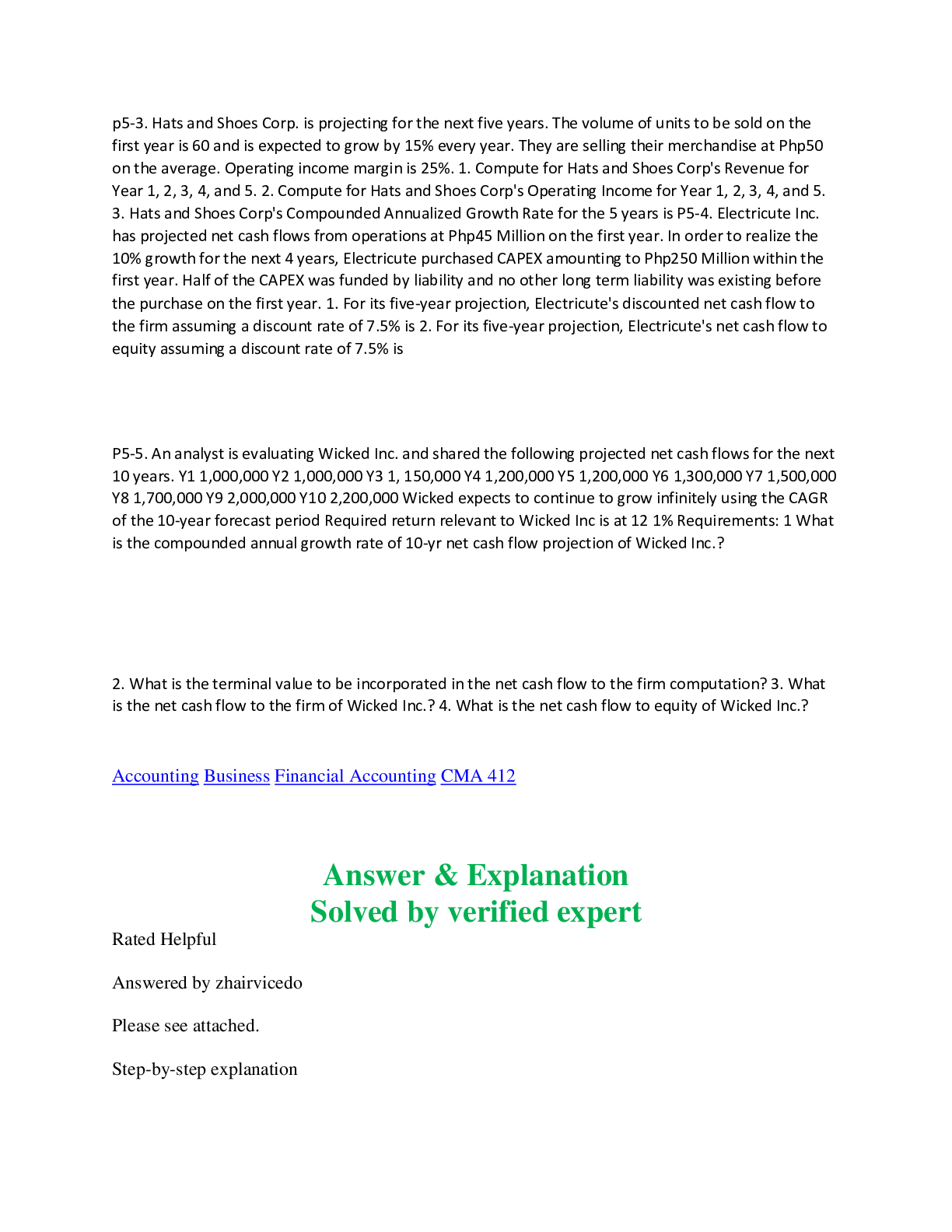

CMA 412 p5-3. Hats and Shoes Corp. is projecting for the next...

Question — Class Notes, Study Guide & Test Bank (Practice Ques...

Pearson RBT Exam — Class Notes, Study Guide & Test Bank (Regis...

Intro Physics MCAS — Strategies for Success | Class Notes, Stu...

NUR2459 / NUR 2459: Final Exam Lecture Notes Updated Mental an...

PN3-Exam-3- Study Guide 1 (complete A+ guide) 100% helpful for...

ATI NCLEX Predictor Remediation Study Notes (2019) Complete A+...

“History of Nursing Complete Notes (Ancient to Modern Nursing,...

NR 566 / NR566 Advanced Pharmacology Care of the Family Weeks...

NR 566 / NR566 Advanced Pharmacology Care of the Family Weeks...