According to PCAOB Auditing Standard

No. 5 (AS 5), the auditor should identify

significant accounts and disclosures and

their relevant assertions. Which of the

following financial statement assertions

is not explici

...

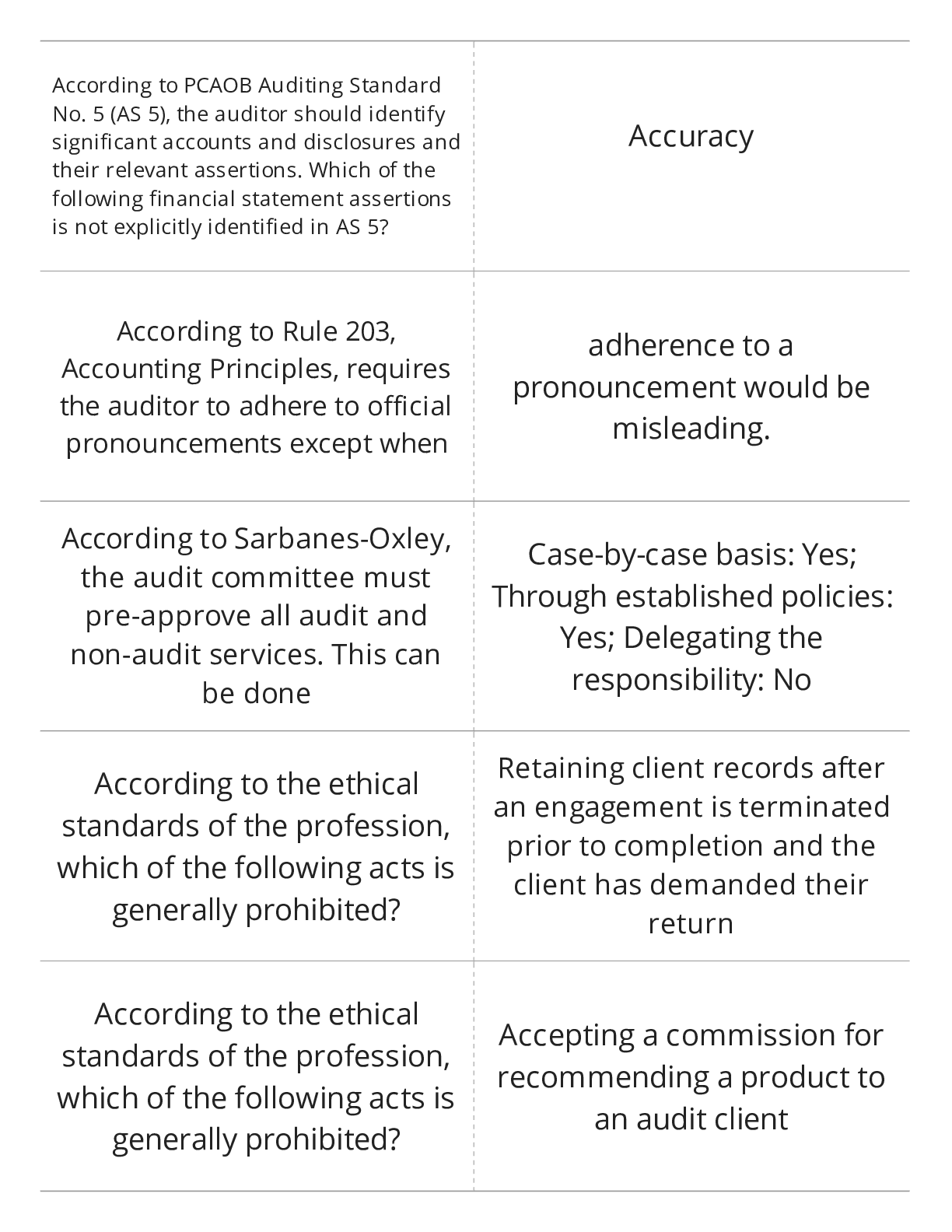

According to PCAOB Auditing Standard

No. 5 (AS 5), the auditor should identify

significant accounts and disclosures and

their relevant assertions. Which of the

following financial statement assertions

is not explicitly identified in AS 5?

Accuracy

According to Rule 203,

Accounting Principles, requires

the auditor to adhere to official

pronouncements except when

adherence to a

pronouncement would be

misleading.

According to Sarbanes-Oxley,

the audit committee must

pre-approve all audit and

non-audit services. This can

be done

Case-by-case basis: Yes;

Through established policies:

Yes; Delegating the

responsibility: No

According to the ethical

standards of the profession,

which of the following acts is

generally prohibited?

Retaining client records after

an engagement is terminated

prior to completion and the

client has demanded their

return

According to the ethical

standards of the profession,

which of the following acts is

generally prohibited?

Accepting a commission for

recommending a product to

an audit client

According to the profession's

ethical standards, an auditor

would be considered

independent in which of the

following instances?

The auditor's checking

account that is fully insured

by a federal agency is held at

a client financial institution.

The accounting, auditing, and

investigating agency of the U.S.

Congress, headed by the U.S.

Comptroller General is known

as

the U.S. General

Accountability Office (GAO).

The AICPA Council has

designated the following bodies

to pronounce accounting

principles under Rule 203,

except the

Auditing Procedures Board.

All of the following are

examples of procedures a

firm can use to monitor its

system of quality control

except

devoting sufficient resources

to developing a system of

quality control.

All of the following statements

are true regarding generally

accepted auditing standards

(GAAS) except

departures from auditing standards

that impose presumptively

mandatory requirements on

auditors are not permitted under

any circumstances.

As it relates to audit

evidence, appropriateness

refers to the

quality of evidence gathered.

Assurance is...

-improving the quality of

information

-for decision makers

Assurance services involve all

of the following, except

providing absolute rather

than reasonable assurance.

An attestation engagement is

one in which a CPA is

engaged to...

issue, or does issue, a report on

subject matter or an assertion

about the subject matter that is

the responsibility of another

party.

Attestation is...

-a practitioner is engaged

-to issue a report on subject

matter or an assertion

-that is the responsibility of

another party

An audit client hires a member

of the audit engagement team

to be its new controller.

Sarbanes-Oxley rules require

that

the client find a new audit

firm.

Audit evidence is usually

considered sufficient when

there is enough quantity to

afford a reasonable basis for

an opinion on financial

statements.

The audit failures of both Enron and

WorldCom were examples in which

the leadership responsibilities for

quality work within the accounting

firm were overshadowed by fears

that losing a key client would

negatively impact individual

auditors' performance

evaluations.

Auditing is...

-systematic process of

obtaining and evaluating

evidence regarding assertions

made by management

The audit objective that all

balances include all items that

should be recorded in that account

is related most closely to which

one of the ASB balance assertions?

Completeness

The audit objective that all

balances include items owned

by the client is related most

closely to which one of the ASB

balance assertions?

Rights and obligations

The audit objective that all the

transactions and accounts presented in

the financial statements represent real

assets, liabilities, revenues, and

expenses is related most closely to

which of the PCAOB assertions?

Existence or occurrence

The audit objective that all

transactions and accounts that

should be presented in the financial

statements are in fact included is

related to which of the PCAOB

assertions?

Completeness

The audit objective that all

transactions are recorded in the

proper account is related most

closely to which one of the ASB

transaction assertions?

Classification

The audit objective that all

transactions are recorded in the

proper period is related most

closely to which of the Audit

Standards Board (ASB) transaction

assertions?

Cutoff

The audit objective that footnotes in the

financial statements should be clear and

expressed such that the information is easily

conveyed to the readers of the financial

statements is related most closely with which

of the ASB presentation and disclosure

assertions?

Understandability

An audit of the financial

statements of Camden

Corporation is being conducted by

external auditors. The external

auditors are expected to

give an opinion on the fair

presentation of Camden's financial

statements in conformity with the

applicable financial reporting

framework (e.g., GAAP, IFRS).

An auditor has substantial doubt about

the entity's ability to continue as a going

concern for a reasonable period of time

because of negative cash flows and

working capital deficiencies. Under

these circumstances, the auditor would

be most concerned about the

possible effects on the

entity's financial statements

An auditor selected items for test counts from

the client's warehouse during the physical

inventory observation. The auditor then traced

these test counts into the detailed inventory

listing that ultimately agreed to the financial

statements. This procedure most likely provided

evidence concerning management's assertion of

completeness.

An auditor selected items from the client's detailed

inventory listing (that agreed to the financial

statements). During the physical inventory observation,

the auditor then found each item selected and counted

the number of units on hand. Assuming that the amount

on hand was the same as the amount in the client's

detailed inventory listing, this procedure most likely

would provide evidence concerning management's

assertion of

existence

The auditor's judgment concerning

the overall fairness of the

presentation of financial position,

results of operations, and cash

flows is applied within the

framework of

the applicable financial

reporting framework (i.e.,

GAAP in the United States).

The auditors' responsibility to

express an opinion on the

financial statements is

explicitly represented in the

introductory paragraph of the

auditors' standard report.

Auditors try to achieve

independence in appearance

in order to

maintain public confidence in

the profession.

An auditor traces the serial

numbers on equipment to a

nonissuer's sub-ledger. Which of

the following management

assertions is supported by this test?

Completeness

Audit Quality Control

-SQCS 8 - specifies six elements

--Leadership 'tone' at the top

--Compliance to relevant ethical requirements

--Acceptance and continuance of engagements

--Human resources

--Engagement performance

--Monitoring

Based on Sarbanes-Oxley,

who is ultimately responsible

for the independence of the

external auditor?

The audit committee

Because of the risk of material

misstatement, an audit of financial

statements in accordance with

generally accepted auditing

standards should be planned and

performed with an attitude of

professional skepticism.

A client has omitted a significant disclosure

from the financial statements. The auditor has

asked the client to include the information,

but the client refuses and claims the

information is confidential. The position of the

CPA should be that the information

cannot be considered

confidential if it is necessary

to the completeness of the

financial statements.

The concept of _________

recognizes that a GAAS audit

may fail to detect all material

misstatements.

reasonable assurance

[Show More]

.png)

(1).png)